With the cost of homes steadily rising, it wouldn’t be surprising if people were looking for a way to save even the smallest amount of money on their home purchase. And between the down payment, closing costs, inspections, PMI, and more, the cost of a home can quickly add up.

With the cost of homes steadily rising, it wouldn’t be surprising if people were looking for a way to save even the smallest amount of money on their home purchase. And between the down payment, closing costs, inspections, PMI, and more, the cost of a home can quickly add up.

Paying interest on your mortgage isn’t avoidable, but you don’t have to feel like you don’t have any control over how much you pay. As you start the homebuying process, you’ll want to consider what factors into the total cost of your loan. The reason being you can improve your chances of saving some cash, especially when it comes to your interest rate.

To ensure you can get the best deal possible, it would be beneficial to understand how mortgage interest works as well as how lenders determine your mortgage interest rate.

How does mortgage interest work?

Mortgage interest, which is a fee charged by a lender for lending money to a borrower, will vary from person to person and lender to lender. Every month when you make your mortgage payment, mortgage interest will account for a portion of that payment. In fact, a majority of the payment is used to pay down interest, while only a small portion is used to pay down the principal balance, or the loan amount.

However, as you continue to make loan payments, and the principal balance decreases, your interest will also decrease. With this change in the amount of interest that is to be paid, more of your payment will go towards the principal balance. With the mortgage interest rate having an impact on the total cost of the loan and your monthly payments, a lower interest rate is better.

What factors affect my mortgage interest rate?

Your lender determines your mortgage interest rate. They do so using a variety of factors that will ultimately help them get a clear picture of your finances and your ability to repay the loan.

Lenders will use seven different factors to determine the mortgage interest rate:

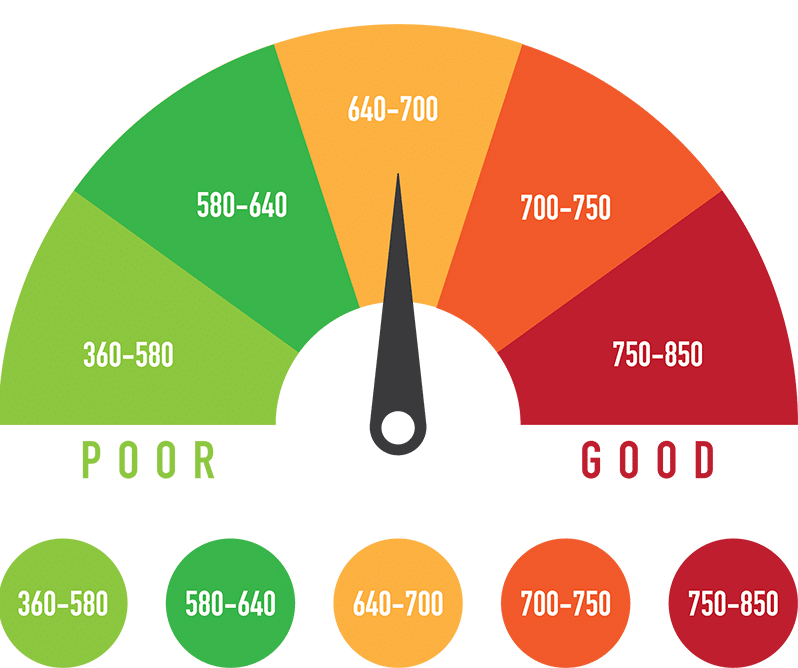

- Credit score: Number used to confirm a consumer’s creditworthiness.

- Home location: State of home.

- Loan type: Conventional, VA, FHA, or other special loan programs.

- Loan amount: The total cost of the home and closing costs minus the down payment.

- Loan term: The time borrowers have to repay their loan.

- Down payment: A percentage of the loan amount paid at closing.

- Type of interest rate: Fixed interest rate stays the same, while adjustable interest rate changes based on the market.

Using the abovementioned factors, lenders will be able to determine your interest rate. Every lender will offer a range of mortgage interest rates, so before applying, you may be able to confirm the rates offered to get a better idea of what the total cost of your mortgage might be.

For example, if a lender’s rates fall between 3.40% and 9.22%, your rate will be between 3.40% and 9.22%. Using a mortgage calculator, you can calculate the cost of your loan and your monthly payments. Of course, if a lender’s rates are too high, you have the option to shop around and look into other lenders who offer something more affordable for your budget.

Next to buying a car, buying a home is likely one of the largest purchases you will make in your lifetime. You might even buy more than one, but as a first-time homebuyer, you may not be 100% sure how to get the best deal. And considering how much people pay in interest, you want to be sure you are getting the best deal.