Divorces are complicated, even more so when you are tied together financially. Not only are you worried about divvying up your assets, but you need to look at dividing up your liabilities too. Unfortunately, in some cases, the divorce decree doesn’t hold power enough to force a lender into revising the terms of a mortgage or loan agreement to release action unless it agrees so in writing.

If you are left trying to pick up and separate the pieces following a divorce, you are not alone. In fact, an average of 800,000 people get divorced every year (630k divorces to 1.6m marriages in 2020.) If you have recently been divorced, one of your number one goals is removing yourself from items that aren’t your responsibility anymore, such as a mortgage or car loan.

Cooperation

First and foremost you are going to need some level of cooperation between both parties. If you didn’t include loan responsibility in your divorce agreement, there’s not a lot you can do without an agreement from the other side. Your former spouse needs to work with you on developing a solution to separate the financial responsibilities of certain assets.

Loan Assumption

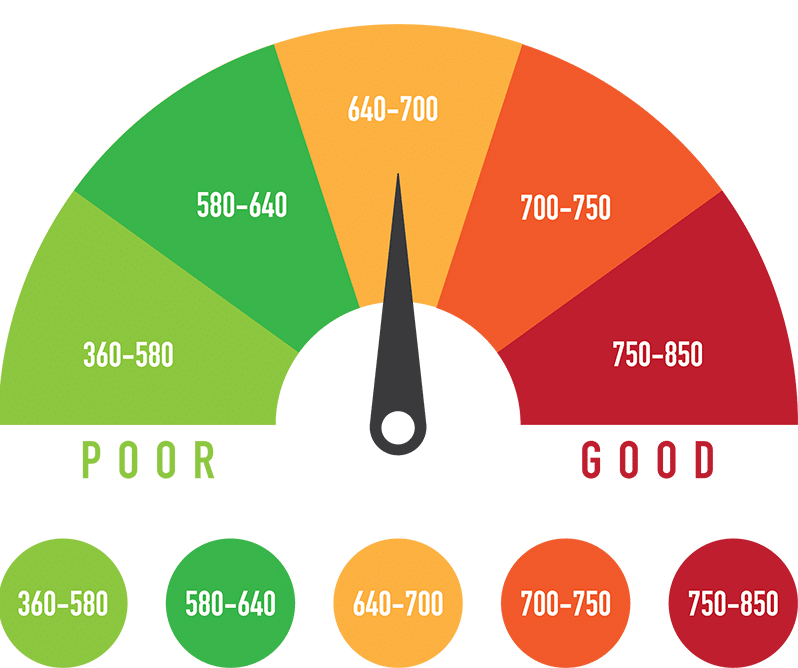

The laws on loan assumption vary from state to state. In order for your former spouse to assume a mortgage in his or her name, they will have to qualify individually for the loan. Just like other loans, your debt and credit score, in addition to a current appraisal, quitclaim deed, and pay assumption will all be taken into account. Once you have lender consent your spouse may assume the existing loan.

Try Refinancing

If loan assumption isn’t an option through your lender the next step is trying to refinance with another mortgage company. In some cases, this may be more beneficial, particularly if payments and interest rates are more affordable. The previous mortgage would be paid with the opening of the new loan, releasing you from debt responsibility. Closing costs might be higher than with assumption. However, this may or may not be possible depending on your former spouse’s financial standing.

Selling the House

The easiest way to put your joint debt behind you is to sell your home and split the equity. In the current market, this may be easier said than done, especially if you happen to owe more on your mortgage than your home is worth. In this case, you would have to pay the difference or opt for a short sale. A short sale is when the sale of your property falls short of the debts owed. In some cases, your lienholder may accept the lesser amount and the sale can be accomplished.

Agree to a Provision

Last but not least, if your former spouse agrees to a provision in writing, you may be able to return to the judge and add it to your decree. This could include something like: if your spouse doesn’t refinance in the next 2-3 years, then the house is to be sold on the market. Conditions such as this give your spouse ample time to figure out a refinancing solution and a fallback if they are not able to.

When it comes to loan repayment, most lenders see two incomes as better than one. This is especially true when it comes to mortgage payments, making it more difficult to separate yourself from your former spouse and your joint liabilities. However, with the right cooperation from both parties, it just might be possible to modify or remove yourself from past agreements. Don’t be afraid to explore your options and ask your lawyer or a debt professional for guidance.