Better Business Bureau

Accredited Business

A+ Rating

Expertise.com

Best Credit Repair

Companies in Phoenix, 2021

Business Hall of Fame

9 Consecutive Years

Best of 2023, Scottsdale

Share Your

Credit Challenges

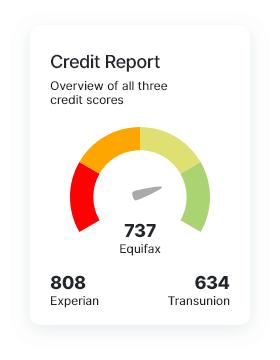

By sharing your goals, we can identify the most efficient credit plan to maximize your credit scores and improve your credit profile.

Complete Complimentary

Credit Analysis

A 30-minute one-on-one in depth review of your entire credit report with our credit experts to ensure we reach your goals as quick as possible.

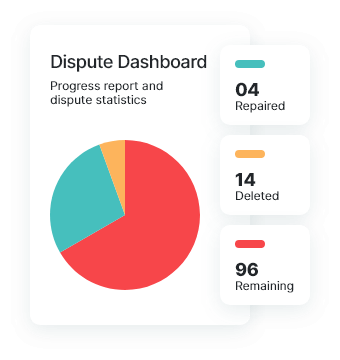

Improve

Your Credit Score

Start utilizing our tools and resources in your personal dashboard to build credit while we take care of the heavy lifting with the credit bureaus.